Tag: VIX

The year is over in a few hours and I thought it would be nice to do a quick review of the year, revisit some studies and the most popular posts of the year, as well as share some thoughts on my performance in 2013 and my goals for 2014.

Revisiting Old Studies

IBS

IBS did pretty badly in 2012, and didn’t manage to reach the amazing performance of 2007-2010 this year either. However, it still worked reasonably well: IBS < 0.5 led to far higher returns than IBS > 0.5, and the highest quarter had negative returns. It still works amazingly well as a filter. Most importantly the magnitude of the effect has diminished. This is partly due to the low volatility we’ve seen this year. After all IBS does best when movements are large, and SPY’s 10-day realized volatility never even broke 20% this year. Here are the stats:

UDIDSRI

The original post can be found here. Performance in 2013 hasn’t been as good as in the past, but was still reasonably OK. I think the results are, again, at least partially due to the low volatility environment in equities this year.

UDIDSRI performance, close-to-close returns after a zero reading.

DOTM seasonality

I’ve done 3 posts on day of the month seasonality (US, EU, Asia), and on average the DOTM effect did its job this year. There are some cases where the top quarter does not have the top returns, but a single year is a relatively small sample so I doubt this has any long-term implications. Here are the stats for 9 major indices:

Day of the month seasonality in 2013

VIX:VXV Ratio

My studies on the implied volatility indices ratio turned out to work pretty badly. Returns when the VIX:VXV ratio was 5% above the 10-day SMA were -0.03%. There were no 200-day highs in the ratio in 2013!

Performance

Overall I would say it was a mixed bag for me this year. Returns were reasonably good, but a bit below my long-term expectations. It was a very good year for equities, and my results can’t compete with SPY’s 5.12 MAR ratio, which makes me feel pretty bad. Of course I understand that years like this one don’t represent the long-term, but it’s annoying to get beaten by b&h nonetheless.

Some strategies did really well:

Others did really poorly:

Others did really poorly:

The Good

Risk was kept under control and entirely within my target range, both in terms of volatility and maximum drawdown. Even when I was at the year’s maximum drawdown I felt comfortable…there is still “psychological room” for more leverage. Daily returns were positively skewed. My biggest success was diversifying across strategies and asset classes. A year ago I was trading few instruments (almost exclusively US equity ETFs) with a limited number of strategies. Combine that with a pretty heavy equity tilt in the GTAA allocation, and my portfolio returns were moving almost in lockstep with the indices (there were very few shorting opportunities in this year’s environment, so the choice was almost always between being long or in cash). Widening my asset universe combined with research into new strategies made a gigantic difference:

The Bad

I made a series of mistakes that significantly hurt my performance figures this year. Small mistakes pile on top of each other and in the end have a pretty large effect. All in all I lost several hundred bp on these screw-ups. Hopefully you can learn from my errors:

- Back in March I forgot the US daylight savings time kicks in earlier than it does here in Europe. I had positions to exit at the open and I got there 45 minutes late. Naturally the market had moved against me.

- A bug in my software led to incorrectly handling dividends, which led to signals being calculated using incorrect prices, which led to a long position when I should have taken a short. Taught me the importance of testing with extreme caution.

- Problems with reporting trade executions at an exchange led to an error where I sent the same order twice and it took me a few minutes to close out the position I had inadvertently created.

- I took delivery on some FX futures when I didn’t want to, cost me commissions and spread to unwind the position.

- Order entry, sent a buy order when I was trying to sell. Caught it immediately so the cost was only commissions + spread.

- And of course the biggest one: not following my systems to the letter. A combination of fear, cowardice, over-confidence in my discretion, and under-confidence in my modeling skills led to some instances where I didn’t take trades that I should have. This is the most shameful mistake of all because of its banality. I don’t plan on repeating it in 2014.

Goals for 2014

- Beat my 2013 risk-adjusted returns.

- Don’t repeat any mistakes.

- Make new mistakes! But minimize their impact. Every error is a valuable learning experience.

- Continue on the same path in terms of research.

- Minimize model implementation risk through better unit testing.

Most Popular

Finally, the most popular posts of the year:

- The original IBS post. Read the paper instead.

- Doing the Jaffray Woodriff Thing. I still need to follow up on that…

- Mining for Three Day Candlestick Patterns, which also spawned a short series of posts.

I want to wish you all a happy and profitable 2014!

Read more 2013: Lessons Learned and Revisiting Some Studies

Part 1 covered the relation between VIX/WVF extreme movements and SPY; here we take a wider look, covering a large number of international equity ETFs.

The main idea behind WVF is that it acts similarly to VIX in high-volatility situations, possibly enough to serve as an implied volatility substitute in cases where such an index does not exist. It can be useful to “confirm” signals based on implied volatility, or to replace them completely in cases where no implied volatility index exists. First of all let’s take a look at an updated VIX & SPY WVF chart:

VIX & SPY WVF

The first post was a while ago, so let’s check how VIX and WVF have performed for SPY since then. The number of signals is very small, and WVF alone has underperformed compared to its historical results, but once again we see that the combination of VIX and WVF offered by far the best results:

Signal results on SPY since 25 Oct. 2012

Let’s take a look at how these signals work internationally:

Close-to-close returns following 100-day 99th percentile VIX return.

It’s clear that using only VIX is pretty useless. Overall the returns are not significantly different from zero, and are even negative in many cases. Let’s check out WVF, which appears to work far better across most ETFs:

Close-to-close returns following 100-day 99th percentile WVF change.

Finally, when VIX and WVF extreme movements coincide, the results look fantastic:

Simultaneous VIX and WVF extreme movements.

Note that even in cases where WVF alone did not show good results (the VT and WVF ETFs for example), combining VIX and WVF still results in great improvement. There is an important, general lesson here about using non-price data as trade set-ups. With few exceptions, implied volatility, breadth, seasonality, etc. need to be “confirmed” by price to actually be useful.

Read more Equity Returns Following Extreme VIX and WVF Movements, Part 2

A simple post on position sizing, comparing three similar volatility-based approaches. In order test the different sizing techniques I’ve set up a long-only strategy applied to SPY, with 4 different signals:

On top of that sits an IBS filter, allowing long positions only when IBS is below 50%. A position is taken if any of the signals is triggered. Entries and exits at the close of the day, no stops or targets. Results include commissions of 1 cent per share.

Sizing based on realized volatility uses the 10-day realized volatility, and then adjusts the size of the position such that, if volatility remains unchanged, the portfolio would have an annualized standard deviation of 17%. The fact that the strategy is not always in the market decreases volatility, which is why to get close to the ~11.5% standard deviation of the fixed fraction sizing we need to “overshoot” by a fair bit.

The same idea is used with the GARCH model, which is used to forecast volatility 3 days ahead. That value is then used to adjust size. And again the same concept is used with VIX, but of course option implied volatility tends to be greater than realized volatility, so we need to overshoot by even more, in this case to 23%.

Let’s take a look at the strategy results with the simplest sizing approach (allocating all available capital):

Top panel: equity curve. Middle panel: drawdown. Bottom panel: leverage.

Returns are the highest during volatile periods, and so are drawdowns. This results in an uneven equity curve, and highly uneven risk exposure. There is, of course, no reason to let the market decide these things for us. Let’s compare the fixed fraction approach to the realized volatility- and VIX-based sizing approaches:

These results are obviously unrealistic: nobody in their right mind would use 600% leverage in this type of trade. A Black Monday would very simply wipe you out. These extremes are rather infrequent, however, and leverage can be capped to a lower value without much effect.

With the increased leverage comes an increase in average drawdown, with >5% drawdowns becoming far more frequent. The average time to recovery is also slightly increased. Given the benefits, I don’t see this as a significant drawback. If you’re willing to tolerate a 20% drawdown, the frequency of 5% drawdowns is not that important.

On the other hand, the deepest drawdowns naturally tend to come during volatile periods, and the decrease of leverage also results in a slight decrease of the max drawdown. Returns are also improved, leading to better risk-adjusted returns across the board for the volatility-based sizing approaches.

The VIX approach underperforms, and the main reason is obviously that it’s not a good measure of expected future volatility. There is also the mismatch between the VIX’s 30-day horizon and the much shorter horizon of the trades. GARCH and realized volatility result in very similar sizing, so the realized volatility approach is preferable due to its simplicity.

Read more Volatility-Based Position Sizing of SPY Swing Trades: Realized vs VIX vs GARCH

The VXV is the VIX’s longer-term brother; it measures implied volatility 3 months out instead of 30 days out. The ratio between the VIX and the VXV captures the differential between short-term and medium-term implied volatility. Naturally, the ratio spends most of its time below 1, typically only spiking up during highly volatile times.

It is immediately obvious by visual inspection that, just like the VIX itself, the VIX:VXV ratio exhibits strong mean reverting tendencies on multiple timescales. It turns out that it can be quite useful in forecasting SPY, VIX, and VIX futures changes.

Short-term extremes

A simplistic method of evaluating short-term extremes is the distance of the VIX:VXV ratio from its 10-day simple moving average. When the ratio is at least 5% above the 10SMA, next-day SPY returns are, on average, 0.303% (front month VIX futures drop by -0.101%). Days when the ratio is more than 5% below the 10SMA are followed by -0.162% returns for SPY. The equity curve shows the returns on the long side:

Long-term extremes

When the ratio hits a 200-day high, next-day SPY returns have been 0.736% on average. Implied volatility does not fall as one might expect, however.

More interestingly, the picture is reversed if we look at slightly longer time frames. 200-day VIX:VXV ratio extremes can predict pullbacks in SPY quite well. The average daily SPY return for the 10 days following a 200-day high is -0.330%. This is naturally accompanied by increases in the VIX of 1.478% per day (the front month futures show returns of 1.814% per day in the same period). It’s not a fail-proof indicator (it picked the bottom in March 2011), but I like it as a sign that things could get ugly in the near future. We recently saw a new 200-day high on the 19th of December: since then SPY is down approximately 1%.

This is my last post for the year, so I leave you with wishes for a happy new year! May your trading be fun and profitable in 2013.

Read more The VIX:VXV Ratio

Introduction

A quick intro to VIX ETPs (some are ETFs, others are ETNs) before we get to the meat: the VIX itself is not tradable, only futures on the VIX are. These futures do not behave like equity index futures which move in lockstep with the underlying, for a variety of reasons. A way to get exposure to these futures without holding them directly, is by using one or more VIX futures-based ETPs. These come in many varieties (long/short, various target average times to expiration, various levels of leverage).

The problem with them, and the reason they fail so badly at mirroring movements in the VIX, is that they have to constantly roll over their futures holdings to maintain their target average time to expiration. A 1-month long ETP will be selling front month futures and buying 2nd month futures every day, for example. Front month futures are usually priced lower than 2nd month futures, which means that the ETP will be losing value as it makes these trades (it’s selling the cheap futures and buying the expensive ones), and vice versa for short ETPs. This amounts to a transfer of wealth from hedgers to speculators willing to take opposite positions; this transfer can be predicted and exploited.

I’ll be looking at two such VIX futures-based instruments in this post: VIXY (which is long the futures), and XIV (which is short the futures). As you can see in the chart below, while the VIX is nearly unchanged over the period, VIXY has lost over 80% of its value. At the same time, XIV is up 50% (though it did suffer a gigantic drawdown).

There are many different approaches to trading these ETPs (for example Mike Brill uses realized VIX volatility to time his trades). The returns are driven by the complex relationships between the value of the index, the value of the index in relation to its moving average, the value of the futures in relation to the index, and the value of various future maturities in relation to each other. These relationships give rise to many strategies, and I’m going to present two of them below.

I’ll be using different approaches for the long and short sides of the trades. Short based on the ratio between the front and 2nd month contract, and long using the basis. Here are the rules:

Go long XIV at close (“short”) when:

- 2nd month contract is between 5% and 20% higher than the front month contract.

Go long VIXY at close (“long”) when:

- Front month future is at least 2.5% below the index.

Finally, if both of the above conditions are triggered, go to cash.

Results

First let’s have a look at how these strategies perform without the hedge. Using data from January 2011 to November 2012, here are the daily return stats for these two approaches individually and when combined:

Equity curves & drawdowns:

The biggest issues with VIX ETN strategies are large drawdowns, and large sudden losses when the VIX spikes up (and to a lesser extent when it spikes down; these tend to be less violent though). A spike in implied volatility is almost always caused by large movements in the underlying index, in this case the S&P 500. We can use this relationship in our favor by utilizing SPY as a hedge.

- When long XIV, short SPY in an equal dollar amount.

- When long VIXY, go long SPY in an equal dollar amount.

The stats:

And the equity curves & drawdowns:

The results are quite good. The bad news is that we have to give up about 40% of CAGR. On a risk-adjusted basis, however, returns are significantly improved.

- CAGR / St. Dev. goes from 38.7 to 45.9.

- CAGR / Max Drawdown goes from 4.5 to 4.9.

All risk measures show significant improvement:

- The worst day goes from a painful -12% to a manageable -9%.

- Maximum drawdown goes from -36.5% to -25.7%.

- Daily standard deviation goes from 4.28% to 2.76%.

Of course, just because risk-adjusted returns are improved does not mean it’s necessarily a good idea. Holding SPY results in both direct costs (commissions, slippage, shorting costs) as well as the opportunity cost of the capital’s next-best use. The improvement may not be enough to justify taking away capital from another system, for example.

Another possibility would be to implement this idea using options, which have the benefit of requiring a small outlay. Especially when holding XIV, SPY puts could be a good idea as both implied volatility and price would move in our direction when the VIX spikes up. However, this must be weighted against theta burn. I don’t have access to a dataset for SPY options to test this out, unfortunately (anyone know where I can get EOD options data that is not absurdly expensive?).

If you want to play around with the data yourself, you can download the spreadsheet here.

Footnotes

Read more Hedging VIX ETP Strategies Using SPY

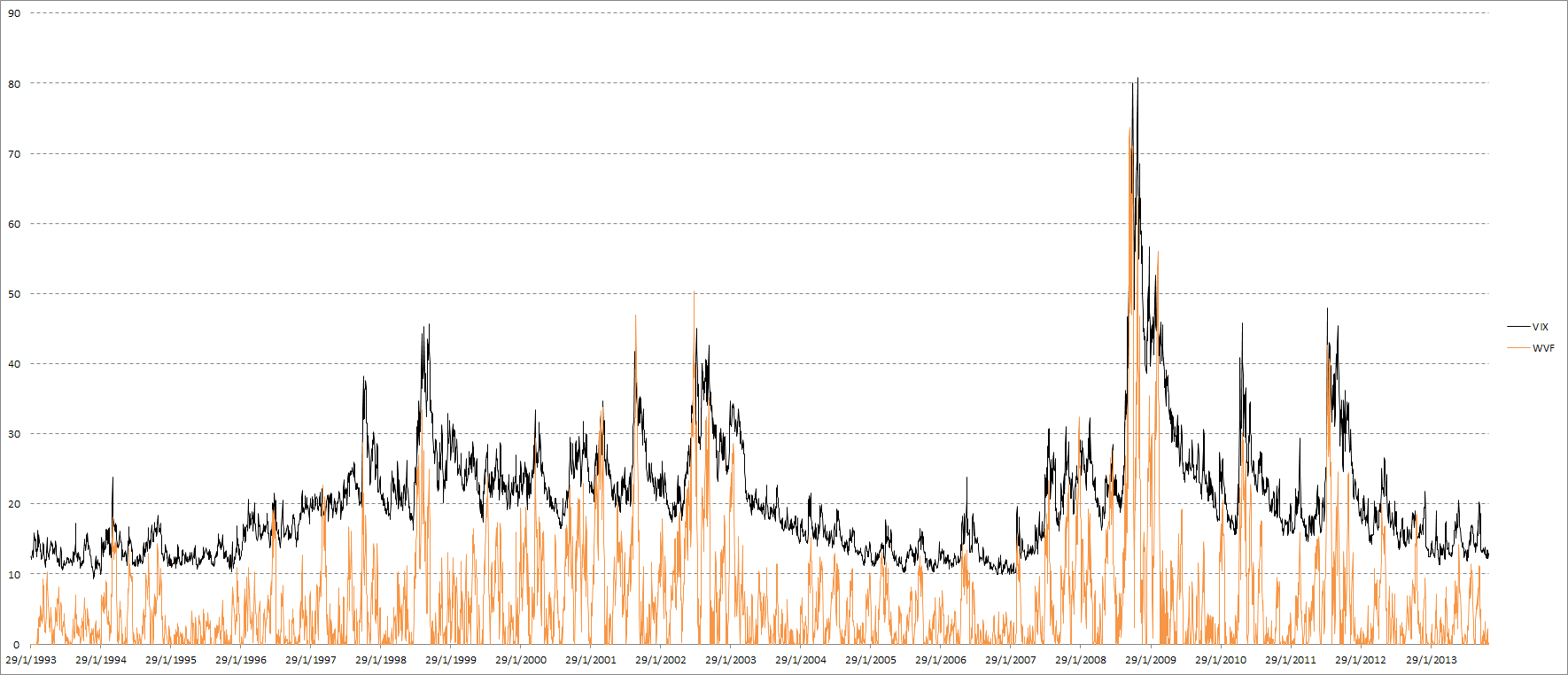

Can extreme changes in implied volatility help predict future returns? And can we use a VIX surrogate as a substitute? First, let’s take a look at the WVF and its relationship to the VIX.

The Williams’ VIX Fix (WVF) is an indicator meant to roughly approximate the VIX. It can be useful in situations where there is no implied volatility index for the instrument we want to trade. The WVF is simply a measure of the distance between today’s close and the 22-day highest close; it is calculated as follows:

A quick visual comparison between the VIX and WVF:

The WVF and VIX behave similarly during volatility spikes, but the WVF fails to emulate the VIX when it hovers at relatively low values. The correlation coefficient between VIX and WVF returns is 0.62, while regressing VIX returns on WVF returns using OLS results in an R2 statistic of 0.38.

We’re not going to be using the level of the VIX and WVF (hardcoding strategies to specific levels of the VIX is generally a terrible idea), so the above chart is somewhat useless for our purposes; we’re going to be looking at the 100-day percentile rank of the daily change. Here is a comparison over a couple of recent months:

Some times they move in lockstep, other times there seems to be almost no relation between them. Still, for such a simple indicator, I would say that the WVF does a fantastic job at keeping up with the VIX.

As you probably know, (implied) volatility is highly mean reverting. Extreme increases in the VIX tend to be followed by decreases. These implied volatility drops also tend to be associated with positive returns for equities. Let’s take a look at simple strategy to illustrate the point:

- Buy SPY on close if the VIX percentage change today is the highest in 100 days.

- Sell on the next close.

Here’s the equity curve and stats:

Nothing spectacular, but quite respectable. Somewhat inconsistent at times of low volatility, but over the long term it seems to be reliable. What about the same approach, but using the WVF instead?

The WVF outperforms the VIX! A somewhat surprising result…the equity curves look similar of course, with long periods of stagnation during low volatility times. Over the long term the stats are quite good, but we might be able to do better…

There is surprisingly little overlap between the VIX and WVF approaches. There are 96 signals from VIX movements, and 109 signals from WVF movements; in 48 instances both are triggered. These 48 instances however are particularly interesting. Here’s a quick breakdown of results depending on which signal has been triggered:

Now this is remarkable. Despite performing better on its own, when isolated the VIX signal is completely useless. This is actually a very useful finding and extends to other similar situations: extreme volatility alone is not enough for an edge, but if used in combination with price-based signals, it can provide significant returns. I leave further combinations on this theme as an exercise for the reader.

A look at the equity curve of “both”:

Long SPY when VIX % change and WVF change are both the highest of the last 100 days, $100k per trade, 1993-2012, no commissions or dividends.

Now that’s just beautiful. You may say “but 37% over 20 years isn’t very impressive at all!”. And you’re right, it isn’t. But for a system that spends almost 99% of the time in cash, it’s fantastic. Want more trade opportunities? Let’s see what happens if we relax the limits on “extremeness”, from the 99th percentile through to the 75th:

Net profit increases, but profitability per trade, and most importantly risk-adjusted returns suffer. The maximum drawdown increases at a much faster rate than net profits if we relax the limits. Still, there could be value in using even the 50th percentile not as a signal in itself, but (like the day of the month effects) as a slight long bias.

Finally, what if we vary the VIX and WVF limits independently of each other? Let’s have a cursory look at some charts:

As expected, the profit factor is highest at (0.99, 0.99), while net profits are highest at the opposite corner of (0.75, 0.75). It’s interesting to note however, that drawdown-adjusted returns are roughly the same both along the (0.99, 0.75-0.99) and (0.75-0.99, 0.99) areas; as long as one of the two is at the highest extremes, you can vary the other with little consequence in terms of risk-adjusted returns, while increasing net profits. This is definitely an area deserving of further analysis, but that’s for another post.

That’s it for now; I hope some of these ideas can be useful for you. In part 2 we’ll take a look at how the above concepts can be applied to international markets, where there is no direct relation to the VIX and there are no local implied volatility indices to use.

Footnotes

Read more Equity Returns Following Extreme VIX and WVF Movements, Part 1

Others did really poorly:

Others did really poorly: