Averaging financial time series in a way that preserves important features is an interesting problem, and central in the quest to create good “alpha curves”. A standard average over several time series will usually smooth away the most salient aspects: the magnitude of the extremes and their timing. Naturally, these points are the most important for traders as they give guidance about when and where to trade.

DTW Barycenter Averaging (or DBA) is an iterative algorithm that uses dynamic time warping to align the series to be averaged with an evolving average. It was introduced in A global averaging method for dynamic time warping, with applications to clustering by Petitjean, et. al. As you’ll see below, the DBA method has several advantages that are quite important when it comes to combining financial time series. Note that it can also be used to cluster time series using k-means. Roughly, the algorithm works as follows:

- The n series to be averaged are labeled S1…Sn and have length T.

- Begin with an initial average series A.

- While average has not converged:

- For each series S, perform DTW against A, and save the path.

- Use the paths, and construct a new average A by giving each point a new value: the average of every point from S connected to it in the DTW path.

You can find detailed step-by-step instructions in the paper linked above.

A good initialization process is extremely important because while the DBA process itself is deterministic, the final result depends heavily on the initial average sequence. For our purposes, we have 3 distinct goals:

- To preserve the shape of the inputs.

- To preserve the magnitude of the extremes on the y axis.

- To preserve the timing of those extremes on the x axis.

Let’s take a look at how DBA compares to normal averaging, and how the initial average sequence affects the end result. For testing purposes I started out with this series:

Then created a bunch of copies by adding some random variation and an x-axis offset:

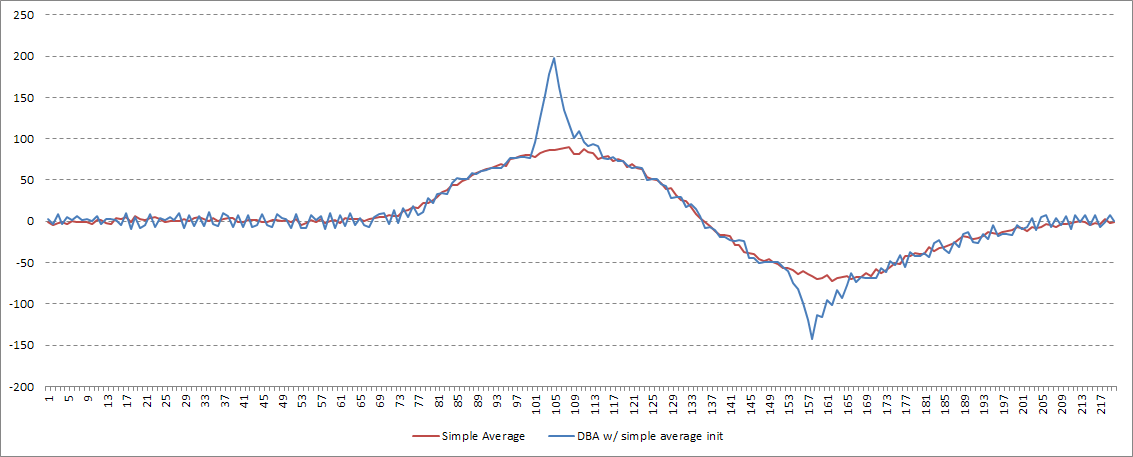

To start out, let’s see what a simple average does. Note the shape, the distance between peak and valley, and the magnitude of the minimum and maximum values: all far from the original series.

The simple average fails at all 3 goals laid out above.

Now, on to DBA. What are our initialization options? My first instinct was to try to start the process using the simple average, above. While this achieves goal #2, the overall shape is obviously wrong.

Petitjean et. al. recommend picking one of the input series at random. On the one hand this preserves the shape well, but the timing of the extremes depends on which series happened to be chosen. Additionally, a deterministic process is preferable for obvious reasons.

My solution was to use an input series for initialization, but to choose it through a deterministic process. I first de-trend every timeseries, then record the x-axis value of the y-axis maximum and minimum values for each series. The series that is closest to the median of those values is chosen. This allows us to preserve the shape, the y-axis extreme magnitudes, and get a good idea of the typical x-axis position of those extremes:

You can find C# code to do DBA here.

Read more Reverse Engineering DynamicHedge’s “Alpha Curves”, Part 2.5 of 3: DTW Barycenter Averaging

DynamicHedge recently introduced a new service called “alpha curves”: the main idea is to find patterns in returns after certain events, and present the most frequently occurring patterns. In their own words, alpha curves “represent a special blend of uniqueness and repeatability”. Here’s what they look like, ranked in order of “pattern dominance”. According to them, they “use different factors other than just returns”. We can speculate about what other factors go into it, possibly something like maximum extension or the timing of maxima and minima, but I’ll keep it simple and only use returns.

In this post I’ll do a short presentation of dynamic time warping, a method of measuring the similarity between time series. In part 2 we will look at a clustering method called K-medoids. Finally in part 3 we will put the two together and generate charts similar to the alpha curves. The terminology might be a bit intimidating, but the ideas are fundamentally highly intuitive. As long as you can grasp the concepts, the implementation details are easy to figure out.

To be honest I’m not so sure about the practical value of this concept, and I have no clue how to quantify its performance. Still, it’s an interesting idea and the concepts that go into it are useful in other areas as well, so this is not an entirely pointless endeavor. My backtesting platform still can’t handle intraday data properly, so I’ll be using daily bars instead, but the ideas are the same no matter the frequency.

So, let’s begin with why we need DTW at all in the first place. What can it do that other measures of similarity, such as Euclidean distance and correlation can not? Starting with correlation: one must keep in mind that it is a measure of similarity based on the difference between means. Significantly different means can lead to high correlation, yet strikingly different price series. For example, the returns of these two series have a correlation of 0.81, despite being quite dissimilar.

A second issue, comes up in the case of slightly out of phase series, which are very similar but can have low correlations and high Euclidean distances. The returns of these two curves have a correlation of .14:

So, what is the solution to these issues? Dynamic Time Warping. The main idea behind DTW is to “warp” the time series so that the distance measurement between each point does not necessarily require both points to have the same x-axis value. Instead, the points further away can be selected, so as to minimize the total distance between the series. The algorithm (the original 1987 paper by Sakoe & Chiba can be found here) restricts the first and last points to be the beginning and end of each series. From there, the matching of points can be visualized as a path on an n by m grid, where n and m are the number of points in each time series.

Source: Elena Tsiporkova, Dynamic Time Warping Algorithm for Gene Expression Time Series

The algorithm finds the path through this grid that minimizes the total distance. The function that measures the distance between each set of points can be anything we want. To restrict the number of possible paths, we restrict the possible points that can be connected, by requiring the path to be monotonically increasing, limiting the slope, and restricting how far away from a straight line the path can stray. The difference between standard Euclidean distance and DTW can be demonstrated graphically. In this case I use two sin curves. The gray lines between the series show which points the distance measurements are done between.

DTW

Euclidean

Notice the warping at the start and end of the series, and how the points in the middle have identical y-values, thus minimizing the total distance.

What are the practical applications of DTW in trading? As we’ll see in the next parts, it can be used to cluster time series. It can also be used to average time series, with the DBA algorithm. Another potential use is k-nn pattern matching strategies, which I have experimented with a bit…some quick tests showed small but persistent improvements in performance over Euclidean distance.

If you want to test it out yourselves, there are plenty of tools out there. I’m using the NDTW .NET library. There are libraries available for R and python as well.

Read more Reverse Engineering DynamicHedge’s Alpha Curves, Part 1 of 3: Dynamic Time Warping

{kind=link}