The QUSMA Data Management System (QDMS) is an application for acquiring, managing, and distributing low-frequency historical and real-time data, written in C#.

QDMS uses a client/server model. The server acts as a broker between clients and external data sources. It also manages metadata on instruments, and local storage of historical data. Finally it also functions as a UI for managing the metadata & data, as well as importing/exporting data from and to CSV files.

Currently it supports two external data sources: Interactive Brokers and Yahoo, but I’ll be adding more in the future.

Note that it’s not “production-ready” right now. There are still a few bugs to iron out, and it also uses unstable 3rd party libraries (the alpha version of the MySQL .NET connector, because it’s the only one that supports Entity Framework 6). All the “core” functionality is implemented and functional, however.

You can find the code here: https://github.com/qusma/qdms. I’m releasing it under the permissive BSD License. Contributions by way of pull requests are more than welcome. If you’d like to make any feature requests or just flame me for the quality of my code, leave a comment right here.

I personally use it in my backtester and portfolio performance evaluation applications, and I’m in the process of integrating it with my live trading app as well.

Using the client is easy, let’s take a look at some code examples:

Getting a list of all instruments:

List<Instrument> instruments = client.FindInstruments();

Searching for a specific instrument, for example SPY:

Instrument spy = client.FindInstruments(new Instrument { Symbol = "SPY" }).FirstOrDefault();

Requesting historical data:

var histRequest = new HistoricalDataRequest(

spy,

BarSize.OneDay,

new DateTime(2013, 1, 1),

new DateTime(2013, 1, 15));

client.RequestHistoricalData(histRequest);

Requesting real time data:

var rtRequest = new RealTimeDataRequest(spy, BarSize.OneSecond); client.RequestRealTimeData(rtRequest);

Some screenshots:

Instrument metadata.

Adding a new instrument from Interactive Brokers.

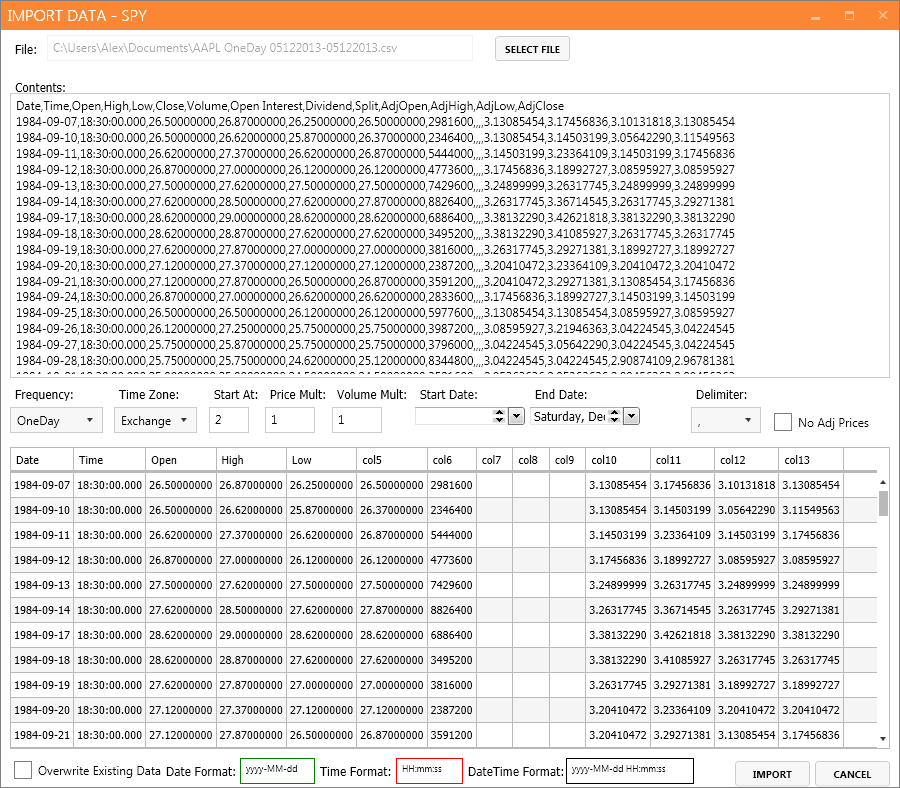

Importing data from a CSV file.

Main server screen.

James says:

Great work! I’ll be looking to contribute in any way I can.

The QUSMA Data Management System Is Now Open Source | Supernova Capital says:

[…] From QUSMA […]

Sayantan Chakraborty says:

hi

i have two question.

1.shall we get benefit for NSE ?

2.can we use it in R?

shirin says:

Thank you for useful information.نمای کامپوزیت

booromand says:

It is an open source data management system? Nice.

راهبند اتوماتیک–کرکره برقی–لامپ کم مصرف–درب ضد سرقت